The OIV's Report about state of Wine Market 2024

If you want read more, you can follow me on Medium where I write about technology news and my personal life.

For technology news click here

My Medium account, here is the place.

This is my X account

The annual report of the OIV (International Organisation of Vine and Wine) shows beyond any doubt that 2024 was another difficult year for the global wine sector.

Adverse weather conditions led to historically low production levels and, at the same time, social and economic factors led to a decline in consumption in key markets.

Despite these pressures, the increase in average prices helped to support the overall performance of the market in terms of value, partly mitigating the impact of the reduction in volumes. This is not necessarily good news, but it is certainly an indicator of how the consumer community is changing.

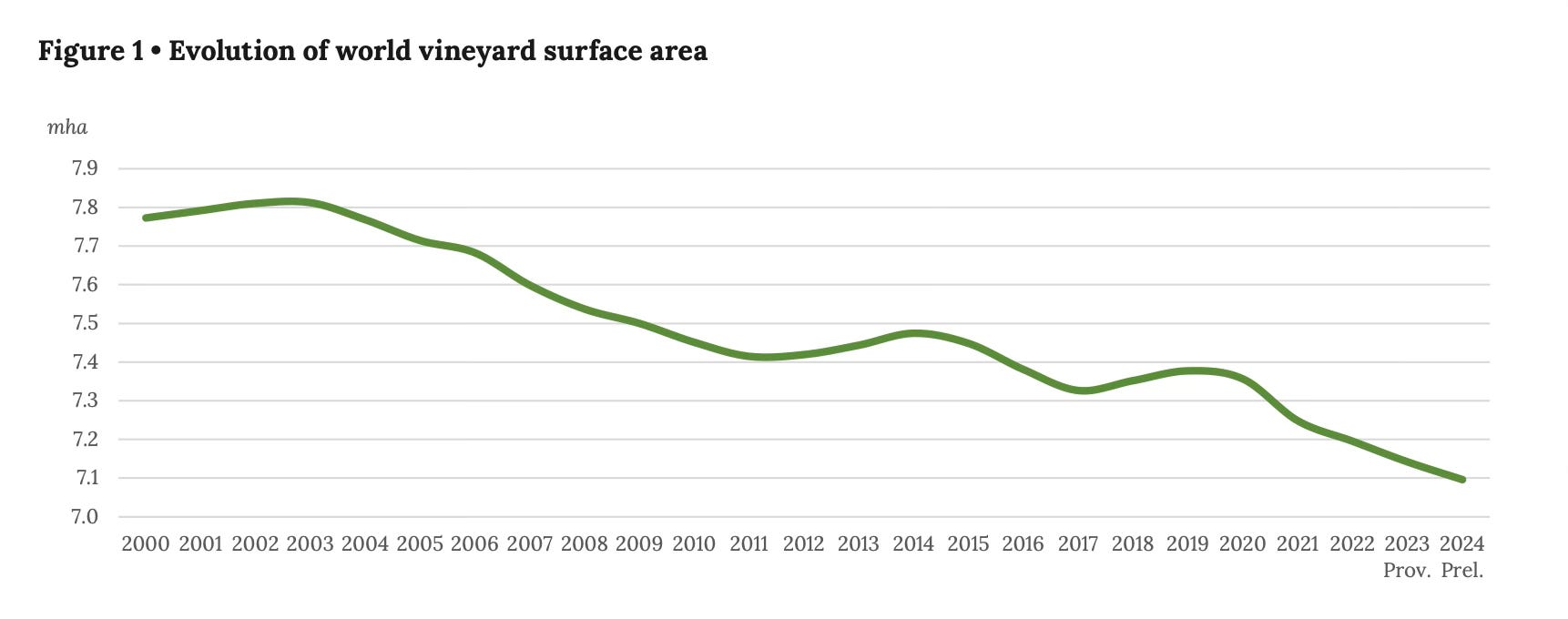

Vineyard area

In 2024, global vineyard area continued to decline, contracting 0.6% to 7.1 million hectares. This marks the fourth consecutive year of decline, driven by the removal of vineyards in major viticultural regions in both hemispheres, affecting all wine grapes and other uses.

European Union

The European Union (EU) recorded an overall decrease of 0.8% in 2024, for a total of 3.2 million hectares. The modest expansions recorded in Italy, Romania and Greece did not compensate for the removals of vineyards observed in other EU countries.

At the national level, Spain, with the largest surface area in the world, has 930 thousand hectares in 2024 and decreased by 1.5% compared to 2023. Likewise, France, with the second largest surface area planted with vines, recorded a decrease of 0.7%, reaching 783,000 hectares. Italy continued its growth, reaching 728,000 hectares.

Rest of the World

In Asia, after a period of significant expansion from 2000 to 2015 (from 300,000 hectares to 770,000 hectares), the vineyard in China, the third largest in the world, has stabilized in recent years and is estimated at 753,000 hectares in 2024 (-0.4%/2023). The USA records 385,000 hectares (-0.7%/2023) and a decline has also been recorded in Argentina and Chile.

Listen the podcast

In South Africa the estimate is 120,000 hectares, with a decrease of 1.5% in 2024, marking the tenth consecutive year of decline. This is attributed in part to the severe droughts that occurred between 2015 and 2017. The vineyard in Australia is estimated at 159,000 hectares, in line with the average observed in the last five years.

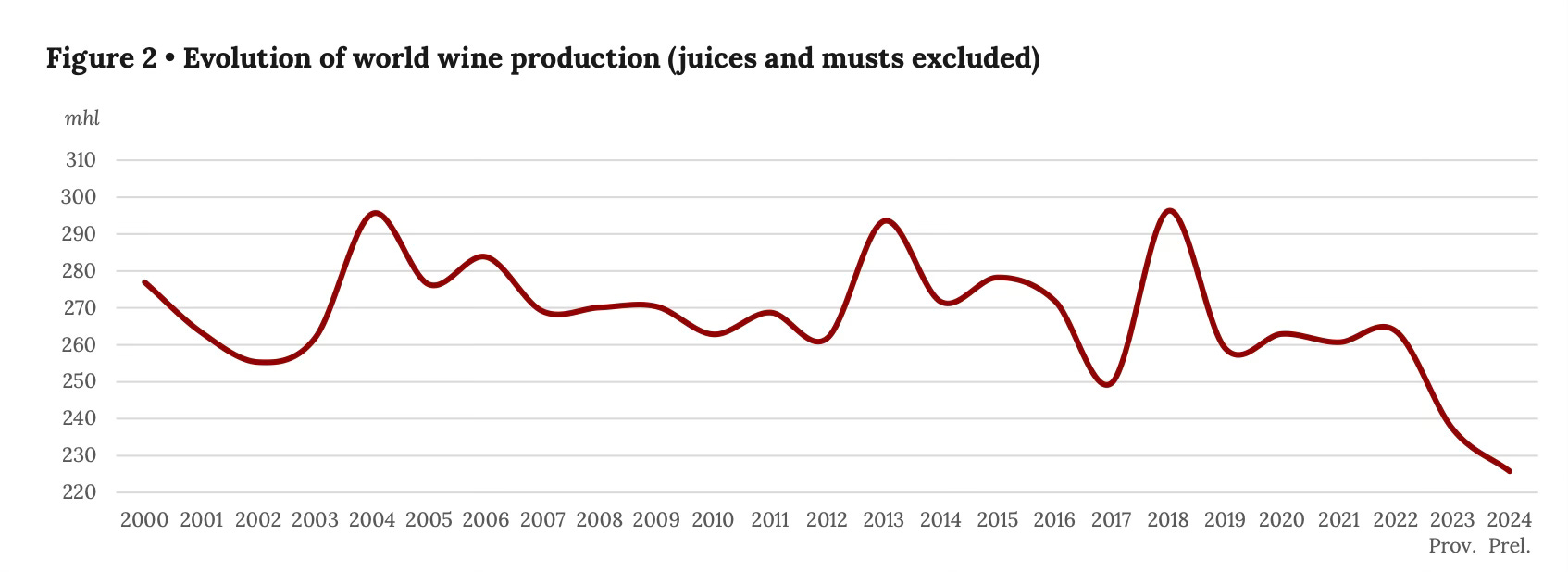

Wine Production

In 2024, world wine production, excluding juices and musts, is estimated at 225.8 million hectoliters, slightly less than the minimum forecast made in November by the OIV (you can check it for comparison from this link), marking a decrease of 4.8% compared to the already historically low production of 2023.

This is the second consecutive year of sharp decline, and the lowest production level recorded since 1961 (219 Million hectoliters), when the spring frost hit the main vineyards of southern Europe, particularly in France.

As in 2023, extreme or atypical weather events are the key influence on global production, with early frosts, heavy rains and prolonged droughts dramatically affecting vineyard productivity.

These factors have severely affected harvest volumes in the main wine-producing regions in both the Northern and Southern Hemispheres. Furthermore, in some regions, this low production reflects market adjustments driven by lower consumption volumes.

Northern Hemisphere

Wine production in the European Union in 2024 is estimated at 138.3 million hectoliters, a decrease of 3.5% compared to 2023. This represents the lowest production volume recorded since the beginning of the century, behind even 2017 (141.5 million hectoliters).

The 2024 data highlights the significant impact of climate change on EU wine regions. While some areas have experienced severe drought and water stress, others have been hit by unprecedented rainfall and destructive storms. These extreme weather conditions have led to an increase in diseases, damage to vineyards and increasingly complicated grape growing conditions.

Italy, the world's largest wine producing nation, is one of the few countries that recorded an average production level in 2024, with 44.1 million hectoliters, which represents a 15% increase compared to 2023, although the 2024 volume is still 6% lower than the average of the last five years.

France produced 36.1 million hectoliters, marking a significant decrease of 11.1 million hectoliters (-23.5%) compared to 2023 and 17.9% lower than its five-year average. This represents the lowest production since 1957 (32.5 million hectoliters).

Spain maintains its position as the world's third largest wine producer, with a production volume of 31 million hectoliters. This represents an increase of 2.6 million hectolitres (+9.3%) compared to 2023, although it remains 11.1% below the five-year average. The increase is driven by relatively positive harvests in Castilla-La Mancha and Extremadura, and is a partial recovery from the severe droughts of 2023, but ongoing water stress continues to challenge winemakers.

Among other major EU countries, Germany, Portugal, Romania and Austria recorded not only a decrease compared to 2023, but also below-average production volumes.

In contrast, Hungary and Greece recorded higher production volumes than in 2023. China's production was 2.6 million hectoliters, down 17.0% from the previous year, while the United States is estimated at 21.1 million hectoliters, down 17.2% from 2023 and 15.5% below the five-year average. In particular, California's harvest was the lowest since 2004.

Southern Hemisphere

The Southern Hemisphere recorded historically low production for the second consecutive year, with production falling to 45.8 million hectoliters, down 3.6% from 2023 and down 13.8% from the five-year average. This is the lowest production level in the last twenty years.

Lower volumes were only recorded at the beginning of the century, when the area devoted to wine grapes was about 15% lower. Most South American countries recorded relatively low production volumes in 2024.

Argentina produced 10.9 million hectoliters, reflecting a significant recovery from a difficult 2023, although still 3.9% below the five-year average. Chile, with a production of 9.3 million hectoliters, recorded a 15.6% decline compared to 2023, the lowest production since 2010 and attributed to a late harvest due to an unusually cool spring and drought conditions in the main wine regions.

South Africa’s 2024 wine production volume was 8.8 million hectolitres, a 5.1% decline from 2023, the lowest production since 2005. The harvest faced multiple challenges, including frost, heavy winter rains, strong winds, flooding and high fungal disease pressure.

Australia’s production was 10.2 million hectolitres in 2024, a 5.3% increase from the historically low 2023 volume but still 16% below the five-year average. New Zealand’s production, at 2.8 million hectolitres, showed a notable decline, 21.2% below 2023 and 13.1% below the five-year average.

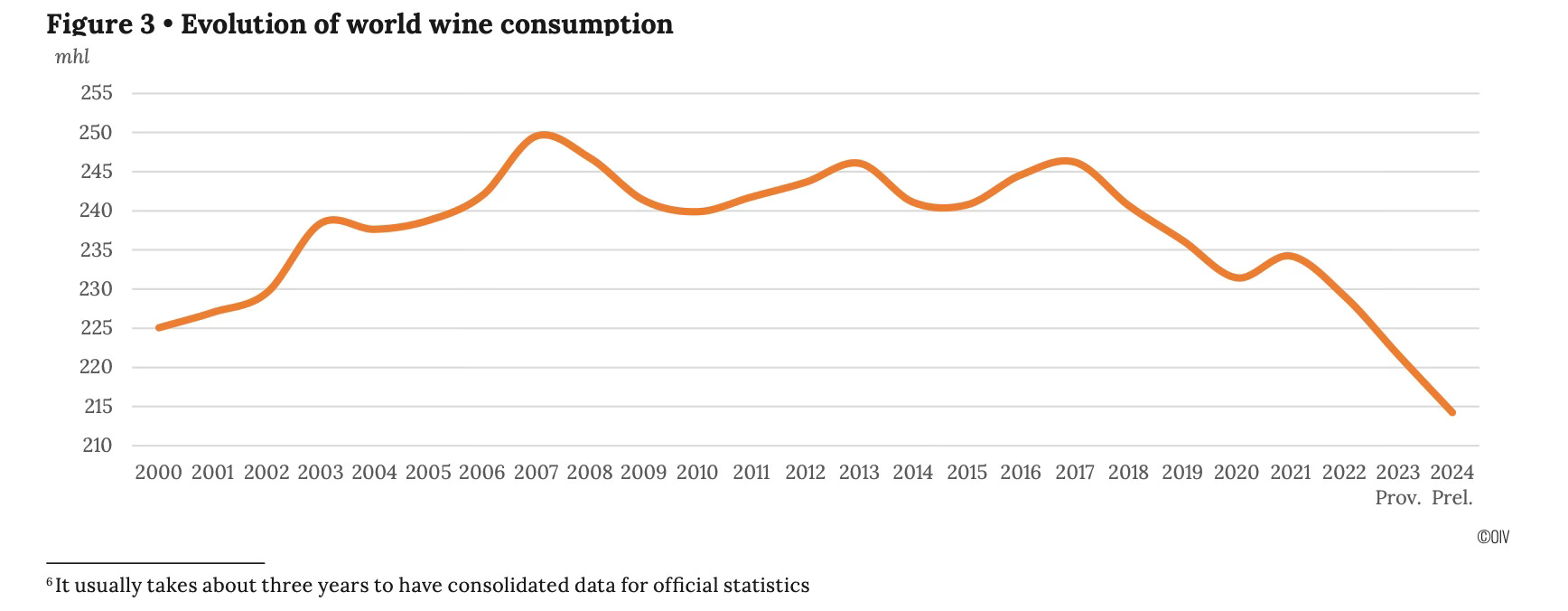

Consumption

2024 confirmed the trend of decline in global wine consumption, with an estimate of 214.2 million hectoliters, down 3.3% compared to 2023. If confirmed, this would be the lowest level recorded since 1961.

Consumption has been decreasing since 2018, and there are many causes, such as the drop in Chinese consumption, on average 2 million hl per year since 2018, and the pandemic in 2020. 2021 and 2022 went better, with the reopening of venues, but then the trend continued to decline.

International political tensions certainly do not help a climate of serenity that pushes people to be together happily with a good glass of wine, but it is not just that. Production costs increased in 2022 because companies had to make up for the losses of 2020-2021, increasing inflationary pressures.

Premium wines, from €20 and up, are doing better than lower-end ones: in practice, who has a good budget for wine can continue to drink medium-high level wines, while everyone else is starting to reduce the quantities of wine purchased.

European Union

EU recorded a consumption of 103,6 M/hl, the 48% of the worldwide consumption and 2,8% less than 2023. The drop is due mainly to fall of consumptions in France, Italy and Germany.

France: 23,0 Mhl (-3,6%)

Italy: 22,3 Mhl (stabile, +0,1%)

Germany: 17,8 Mhl (-3,0%)

Spain: 9,9 Mhl (+1,2%)

Portugal: 5,6 Mhl (+4,7%)

Netherland: 3,2 Mhl (-8,1%)

Romania: 3,0 Mhl (-11%)

Austria: 2,2 Mhl (-2,6%)

Hungary: 2,2 Mhl (+7,5%)

Rest of the World

All major markets are down from 2023, but China is leading the decline over the past five years.

United Kingdom: 12,6 Mhl (-1,0%)

Svitzerland: 2,2 Mhl (-5,0%)

United States: 33,3 Mhl (-5,8%)

Canada: 4,6 Mhl (-6,4%)

China: 5,5 Mhl (-19,3%)

Japan: 3,1 Mhl (-4,4%)

Argentina: 7,7 Mhl (-1,2%)

Brasil: 3,1 Mhl (-4,3%)

South Africa: 4,3 Mhl (-2,8%)

Australia: 5,3 Mhl (-2,7%)

International trade

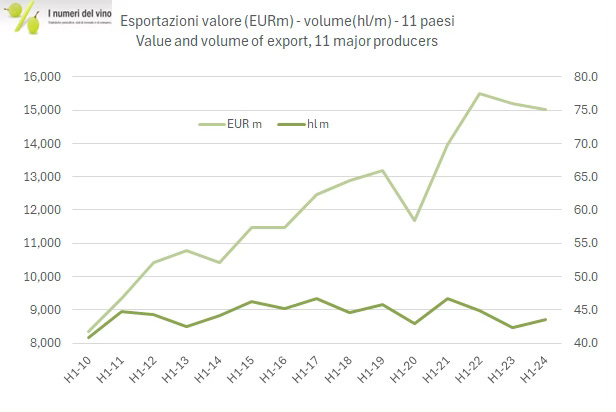

The low production of the last two years, the high average export prices and the increasingly weak international demand for wine have significantly impacted the market in 2024.

International wine exports remain globally at the lowest value since 2010, standing at 99.8 million hl, in line with 2023. Analyzing the various producers, Chile, Australia, Portugal and the United States have shown a slight sign of improvement, but for all the others the negative sign applies.

In this post from I numeri del vino you can see the graph of the export trend up to the first half of 2024: prices are increasing in the face of little change in volumes.

The estimated value of exports is €35.9 billions, only 0.3% less than in 2023, and a stable average price of €3.6/liter, which is decidedly high for this marker.

The cause is in the strategy of pushing premium wines, a strategy that began at least a decade ago and has recently accelerated. In practice, a cluster of consumers is being created who have no problem continuing to buy wine by spending more, while daily wine consumers are decreasing. Not good news for smaller producers. In addition, we must add the general price increases observed since the end of the pandemic to date.

As for the types of wine, in exports, bottled wine (i.e. wine in containers smaller than 2 liters) represents 50.8% of all wine sold, down 1.8% compared to 2023, and 67% in value, stable. For bottled wines, the average price is €4.7/liter, an increase of 1.9% over 2023. Sparkling wines saw a decrease of 3.7% in value, while in volume they remained almost stable (-0.3%), bringing the average export price to €7.9/liter, down 3.4%. Bubbles are 10.9% of all wine exports, and represent almost a quarter of the total value.

The Bag-in-Box category (containers greater than 2 liters but less than 10), represented 3.6% in volume and 1.9% in value of the total, down 5%. The price remained substantially stable at €1.9/liter. Bulk wine exports, i.e. wine sold in containers larger than 10 litres, saw a 3.3% increase in volume and accounted for 34.7% of total bulk exports, and a sharp increase of almost 10% in value, reaching €0.8/litre.

Exporting Countries

The three largest exporters are, as always, Italy, Spain and France, which with a total of 54.6 million hl represent 54.7% of world exports and 63.4% of value. Italy is the largest exporter, in terms of quantity, with 21.7 million hl and €8.1 billion. The good results are mainly due to sparkling wines, Prosecco above all, with a 12% increase in volume.

Spain saw its exports decrease to 20 million hl (-1 million hl), mainly due to the decrease in bulk wine, which still represents 55% of Spanish exports. The value of all exports increased, however, and amounted to €3 billion.

France ranks third in terms of exported quantity, 12.8 million hl, but is far ahead of everyone with €11.7 billion, which is still a lower value than in 2023. Bottled wines remained stable, while sparkling wines saw a decrease of 2.4% in volume and 6.5% in value.

Chile increased its export share by 14.4%, positioning itself at 7.8 million hl for a value of €1.5 billion. Australia saw an increase in exported quantities with 6.5 million hectoliters and €1.6 billion, a performance better than 30.6% compared to 2023, also thanks to the renewed trade with China, especially for bottled wines, which produced 77% of the total export value.

South Africa grew to 3.6 million hectoliters and €0.6 billion, continuing to show signs of weakness especially in bottled wines. Portugal increased to 3.5 million hl exports and €1 billion, one of the best performances in percentage terms. Germany decreased, with 3.1 million hl, as did New Zealand, at 2.7 million hl.

In 2023, the United States saw an increase in exported quantities of 15.5%, which was 2.4 million hl, bringing the value of exports to €1.2 billion, but practically all of the increase was due to bulk wine, which for the USA represents 48% of the exported volume.

Importing Countries

In 2024, the largest wine importers were again Germany, the United Kingdom and the United States, which represent 38.3% of the world import market, generating 37.2% of value.

In this ranking, Germany imports 12.7 million hl, down almost 7% on 2023, the lowest level in the last 20 years. In total, Germany imports wines for €2.5 billion, 8.8% less than in 2023. The United Kingdom has seen an increase in imported wine, reaching 12.6 million hl of which 37% are bulk wines. The value of imports is €4.6 billion.

The United States is positioned at approximately the same import figures, with 12.3 million hl, but is by far the first in terms of the value of imported wines, or €6.3 billion.

Bottled wines have increased, accounting for 56% of the total in quantity, and bulk wines have decreased. France and the Netherlands have decreased their imports, the lowest value since 2016. France imports 5.4 million hl, the Netherlands less than 4 million hl.

In 2023, Italy imported 2.9 million hl, with an increase of 65.6% on 2023 and a value of €0.5 billion, mainly bulk wine, which is 86% of the total volume.

As for China, perhaps the period of decreasing imports, which lasted for six years, is coming to an end. In 2024, 2.8 million hl were imported, an increase of 13.7% on 2023, for a total of €1.5 billion of which 90% is due to bottled wines.